Bruce Henderson published the growth-share matrix in 1970 as a way for diversified corporations to allocate capital across a portfolio of businesses. Two axes — market growth rate on the vertical, relative market share on the horizontal — produced four quadrants that any CEO could read at a glance. Stars in the top-right earned investment. Cash cows in the bottom-right funded that investment. Question marks in the top-left forced a decision. Dogs in the bottom-left were candidates for divestiture. For roughly fifteen years, the matrix was the dominant portfolio tool in the Fortune 500.

Then it went out of fashion. By the mid-1990s the BCG matrix was widely criticized as too simplistic, too dependent on assumptions that had stopped being true, and too easily misused. Business schools kept teaching it as historical context. Consultants replaced it with more elaborate frameworks. Boards moved on. For most of the 2000s and 2010s, if you brought a BCG matrix to a strategy meeting you would be gently told that portfolio thinking had evolved.

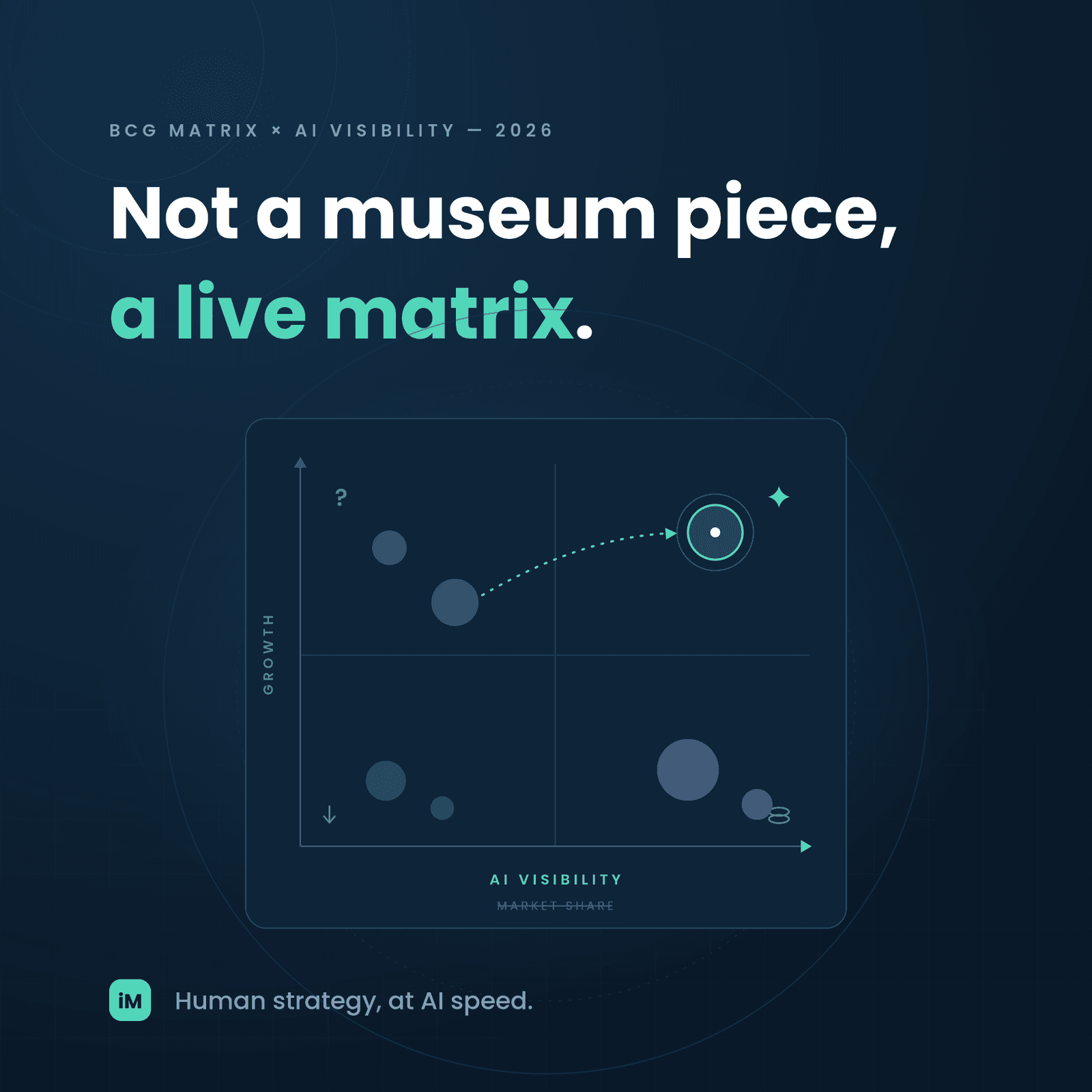

In 2026 the matrix is back — not as nostalgia, but as a working tool. Boards are asking portfolio questions again because the pace of category reshuffling has outrun the annual planning cycle. Multi-brand groups are re-examining which of their brands deserve growth capital and which should be optimized for cash extraction. Challenger-brand holding companies are running matrix reviews quarterly. The framework is coming back, but the two axes are being rebuilt — because measuring "market growth" and "relative market share" with the same instruments Henderson used in 1970 no longer captures the reality of a market where AI-driven discovery is shifting category boundaries faster than revenue data can register.

Why the matrix went out of fashion

Three critiques buried the matrix as a decision tool between 1990 and 2015.

The first critique was capital-markets efficiency. Henderson's original logic assumed that cash cows had to fund stars because external capital was expensive and information-asymmetric. That assumption made sense when the average corporate bond issuance took months and public markets were less transparent. It made progressively less sense as capital markets became more liquid and information-rich. If a star business was truly high-growth with defensible share, the capital markets would fund it directly — the parent company's cash cow was not the only, or even the cheapest, source of capital.

The second critique was strategic focus. The 1990s brought a wave of divestitures and refocusing driven by the argument that diversified conglomerates trade at a discount to their sum-of-parts. If the market is going to discount your diversified portfolio anyway, the portfolio-allocation logic of the BCG matrix becomes secondary to the more urgent question of whether the portfolio should exist at all. Companies broke themselves up. Portfolio thinking was replaced by focus thinking.

The third critique was measurement. The matrix required you to know two things reliably — the market's growth rate and your relative share in a well-defined market. Both got harder as digital transformation blurred category boundaries. What is the market for "office productivity software" when it now includes collaboration, project management, video, transcription, and increasingly AI copilots? What is your relative share in a market whose edges are contested? By the 2010s the input data was so contested that the output quadrant assignment felt arbitrary.

Why the matrix is coming back

The three critiques have not gone away. Capital markets are still efficient. Focus still matters. Category boundaries are still contested. But three new forces have made portfolio thinking urgent again, and the matrix is proving to be the most communicable framework for that thinking.

The first new force is challenger-brand aggregation. The last decade produced a wave of holding companies that own portfolios of digitally-native challenger brands — often ten, twenty, or more brands across adjacent categories. For those groups, the portfolio allocation question is not an occasional strategic exercise. It is the operating cadence. Which brands get the next tranche of marketing spend? Which are quietly harvested? Which are being kept alive out of inertia? The matrix, updated, is proving to be the clearest board-level way to answer those questions.

The second new force is the compression of category life cycles. Categories are being created, expanded, and reshaped faster in 2026 than at any point in the postwar period. A brand that was in a growth category in 2023 can find itself in a maturing one by 2025 as buyer behavior shifts, adjacent categories absorb its use cases, or AI-driven discovery collapses distinctions that used to justify separate categories. Portfolio decisions that used to be reviewed annually now need review quarterly.

The third new force — and this is where the story becomes specific to 2026 — is that AI-driven discovery is now materially altering which categories are growing and which are contracting, in ways that lead the revenue data. When ChatGPT, Perplexity, Gemini, and Claude start recommending a new category framing to buyers, category share can shift months before the shift appears in reported revenue. Boards that wait for revenue confirmation reallocate too late. Boards that read the AI signals reallocate on the leading edge. That is why AI visibility data has become the fastest-moving input to the modernized matrix.

The two axes, rebuilt

The classical matrix used market growth rate on the vertical axis and relative market share on the horizontal. Both axes are still the right conceptual choice. What has to change is how they are measured. In 2026 both axes need to combine slower revenue-derived signals with faster AI-and-digital signals, because the revenue-derived signals alone are too lagged to support quarterly portfolio decisions.

Vertical axis: market growth momentum

Henderson's original vertical axis was market growth rate, typically measured as compound annual growth rate of category revenue. That number is still useful, but it is a trailing indicator — you know your category grew 12% last year, but that tells you little about whether growth is accelerating, decelerating, or about to shift. A modernized vertical axis should combine the trailing revenue-growth number with three leading indicators that can be observed in something closer to real time.

- Category-level digital demand signals — search demand for category terms, social and community conversation volume, and organic content velocity. These typically lead category revenue growth by two to four quarters.

- AI category-recommendation share — how often the major AI engines are recommending the category itself as the answer to buyer problems (independent of which brand is recommended). Rising category-recommendation share is a strong leading indicator of accelerating buyer entry into the category.

- Competitor investment velocity — the rate at which competitors in the category are publishing, expanding sales coverage, and launching adjacent products. This is a competitor-behavior proxy for their internal read of category growth.

The vertical axis is no longer a single number pulled from a market research report. It is a composite that blends the trailing revenue growth with the leading demand and AI signals. A brand can now be plotted vertically with weeks of latency instead of quarters.

Horizontal axis: relative competitive strength

Henderson's original horizontal axis was relative market share, measured as the brand's share divided by the largest competitor's share. That number is still useful, but it captures only one dimension of competitive strength, and in categories where the market is not tightly defined, it can be gameable by choosing the market definition carefully. A modernized horizontal axis should combine relative revenue share with two competitive-position signals that are harder to game and faster to move.

- AI-mention and AI-recommendation share — the share of category-level AI queries in which your brand is mentioned or recommended, benchmarked against your top competitors. This tends to lead shifts in shortlist inclusion, which then leads shifts in revenue share.

- Composite benchmark score — a multi-dimensional competitive assessment that includes brand strength, digital performance, sentiment, and category-specific competitive attributes, expressed relative to the top competitors in the category.

The horizontal axis becomes a composite of a lagging revenue-share number and two leading competitive-position numbers. A brand that is losing AI mention share while still holding revenue share is heading toward a horizontal-axis shift the revenue data has not yet registered. Reading that shift early is the whole point of updating the matrix.

Why dynamic thresholds matter more than the classic 1.0 line

The classical matrix used a fixed threshold — the median for growth, a relative-share of 1.0 for the horizontal cut — to divide the quadrants. Those fixed thresholds were part of the framework's simplicity, but they were also part of its brittleness. A portfolio full of brands in a slow-growth category will show up as all-cash-cows-and-dogs against a fixed threshold, when the portfolio-relevant question is which of those brands are relatively stronger and relatively weaker within the portfolio's own reality.

A modernized matrix uses dynamic thresholds calibrated to the portfolio being analyzed. The vertical cut is the median growth momentum of the portfolio's own units. The horizontal cut is the median composite strength of the portfolio's own units. Quadrant assignments become portfolio-relative, not absolute — and the resulting quadrant reading answers the question the board is actually asking: given the portfolio we have, which units are relatively investable and which are relatively harvestable?

How the CFO and CMO now align

One of the reasons the modernized matrix is spreading is that it gives CFOs and CMOs a shared decision surface. In the classical matrix, the CFO tended to focus on the horizontal axis — revenue share, cash generation, the harder numbers. The CMO tended to focus on the vertical axis — growth, demand, brand momentum. The two conversations happened at different tables and reached different conclusions.

The rebuilt axes include both financial and marketing-derived inputs on each axis. Revenue growth and AI category signals sit together on the vertical. Revenue share and AI mention share sit together on the horizontal. When the CFO and CMO look at the plotted portfolio, they are looking at the same units with the same inputs, and the disagreement — if there is one — is about strategic response, not about whose data is right. That alignment is why boards are gravitating back to the matrix in 2026.

A worked playbook

Step 1 — Define your portfolio units at the right grain

A common failure is running the matrix at the wrong grain. Too coarse (business unit) and you miss the sub-brand dynamics that actually drive allocation decisions. Too fine (product SKU) and you drown in noise. For most multi-brand groups, the right grain is the brand or the sub-brand — the level at which the marketing budget and product roadmap are decided together.

Step 2 — Score both axes as composites, not single numbers

For each portfolio unit, compute the vertical axis as a weighted composite of category revenue growth (lagging), category digital-demand signals (leading), AI category-recommendation share (leading), and competitor investment velocity (leading). Compute the horizontal axis as a weighted composite of relative revenue share (lagging), AI mention share (leading), and composite competitive benchmark score (leading). Document the weights so the matrix can be reproduced next quarter.

Step 3 — Plot with dynamic thresholds

Compute the median vertical and horizontal composite across the portfolio. Draw the quadrant boundaries at those medians. Every unit is now positioned relative to the portfolio's own reality, not against a decades-old absolute cutoff.

Step 4 — Read the quadrants, including the edges

Standard quadrant reads apply. Stars in the top-right earn continued investment. Cash cows in the bottom-right are optimized for margin and cash generation. Question marks in the top-left require an explicit invest-or-exit decision. Dogs in the bottom-left are candidates for divestiture or wind-down. But the more actionable read is often the edge cases — a brand sitting one point below the median on the vertical axis but with strong AI momentum signals is a candidate for reclassification from cow to star, and the response should be a targeted investment rather than continued milking.

Step 5 — Assign strategy per unit and re-run quarterly

Each unit gets a documented strategic assignment — invest, harvest, decide, divest — with a specific set of levers and a quarterly review. The matrix is no longer an annual PowerPoint slide. It is a living portfolio dashboard that shifts as the underlying signals shift, and the strategic assignments update with it.

Common mistakes to avoid

- Running the matrix with only lagging inputs. If both axes are pure revenue-derived numbers, the matrix is at best a rear-view mirror. Blend leading and lagging inputs on each axis or the exercise is directionally wrong.

- Using fixed thresholds against a portfolio that does not match the fixed benchmark. Dynamic, portfolio-relative thresholds are more useful for the allocation decision the board is actually making.

- Treating quadrant labels as terminal. Stars can decelerate into cows. Cows can be reinvested into stars. Question marks resolve into either. Dogs can be repositioned. The label is a starting point for the strategic conversation, not the end of it.

- Confusing the matrix with a resource-allocation formula. The matrix suggests where the strategic case is strongest. It does not replace the case itself. Every quadrant assignment should trigger a specific strategic argument that the board can accept or challenge.

Portfolio thinking is back on boardroom walls not because the classical framework was right but because the questions it asked are urgent again. The axes had to be rebuilt. The reading has to be quarterly. The signals have to include AI. But the framing is right for the moment.

Where inMOLA fits in

The rebuilt BCG matrix requires inputs that most enterprise reporting stacks do not currently combine into a single view. Revenue growth data lives in the finance system. Digital demand signals live in the SEO and web analytics stacks. AI category-recommendation share and AI mention share live in AI visibility monitoring. Competitor benchmark composites live in competitive intelligence platforms. Reconciling those inputs into a single per-brand pair of scores is where most portfolio exercises stall.

inMOLA's BCG Box Matrix module was built to close that gap. It draws on the same competitor benchmark and AI visibility data that flow through the rest of the inMOLA decision engine, computes the composite vertical and horizontal scores per brand, and plots the portfolio with dynamic portfolio-relative thresholds. The output is a matrix a board can read at a glance, backed by data traceable back to source signals. Because the module runs on the same continuously-refreshed data as the AI Visibility and Competitive Intelligence modules, the matrix is not an annual artifact — it updates as the underlying signals update, and the portfolio conversation stays current with the market.

The strategic value of the modernized matrix is not that it changes the four quadrant labels. Those are the same as they were in 1970. The value is that the plotted positions in 2026 reflect leading indicators that boards used to have to wait quarters to see in revenue data. Reading the leading positions early is what enables portfolio reallocation on the leading edge instead of the trailing edge. In 2026, the boards that reallocate on the leading edge compound advantage against the ones still reading the annual review.